For decades, the average American has used mutual funds to grow their money. The typical mutual fund is “actively managed”, which is a great selling point for the fund. Most people think active management will maximize growth when markets are going up, and minimize, or even eliminate, loss when markets are in decline. That’s a common misconception about active wealth management. Here’s why:

The Active Management Misnomer:

While the objective of most index mutual funds is to outperform the market index they’re matched to, most active managers fail to do that, at least from the investor’s perspective. Sure, they experience growth during a bull market; but there’s little or nothing done to protect those gains when markets are bear. So investors can see years of growth disappear when markets go south, sometimes in a very short period of time. The reason is the institutional mandate, which requires managers to manage a fund using a specific strategy and within certain risk parameters. For example, a long-term growth mandate requires the manager to prioritize long-term capital appreciation over things like higher risk for higher return.

Individuals and institutions have different expectations. So while active management may seem like a good feature, that’s not always the case. Institutions expect fund managers to follow their index closely even if it means huge losses in the short-term. The ironic thing is, fund managers can legitimately claim they “out-performed”, even if individual portfolios lost money. That’s because they’re referring to company benchmarks when they make this claim, not portfolio growth or loss.

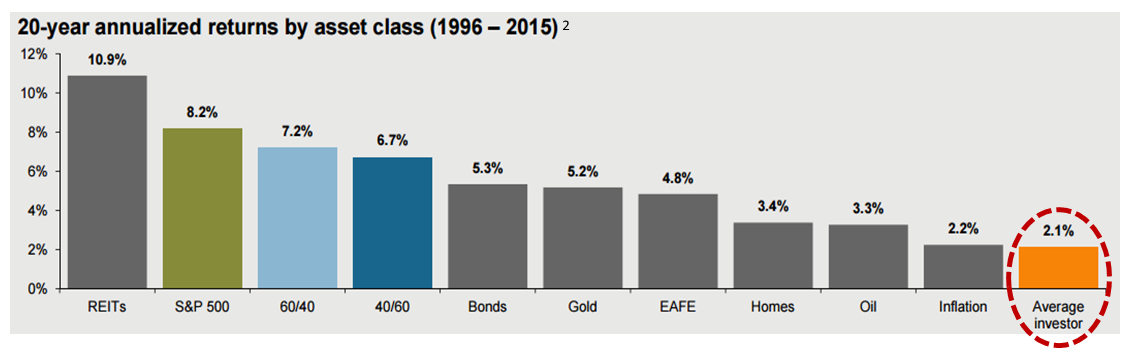

So, even though a fund is actively managed, investors actually have to make buy/sell decisions when markets change. The problem with that scenario is the average person’s buy/sell decisions are based on emotion and, on average, result in returns that are just short of the rate of inflation.

{kind=link}

The Irony of the Prospectus:

Another problem with active management is found in the fund prospectus. Many active funds effectively prohibit selling a large percentage of the portfolio, even though that’s often necessary if you want to protect your gains. The fund manager is required to stay fully or mostly invested because that’s what the fund prospectus says. Ironically, the document that’s intended to protect consumers sometimes lets them down.

An Attractive Alternative

Tactical active management, on the other hand, is better suited to meet the typical investor’s needs and expectations. Tactical active management seeks growth during bull market periods and is designed to avoid, or at least minimize losses found in bear market periods. The reason is tactical managers follow rules-based systems that are designed to protect wealth, guide them through market ups and downs, and do the buying and selling for you.

Of course, no strategy can completely eliminate loss, but active tactical management is a great way to enjoy consistent growth and avoid those catastrophic losses that can take years to recover from.

Contact us today to learn more about building your wealth, and the variety of financial planning options we offer. We also invite you to follow our blog for more useful financial planning content.